Why short duration Asian bonds could be a flexible and well-timed play on market uncertainty?

- 16 September 2020 (5 min read)

Key points

- The ultra-low interest rate environment is driving yield-hunting investors to look east at Asian credit.

- A short duration approach can potentially provide a natural buffer against rising inflationary expectations, and long-term interest rate risks.

- By re-allocating interest rate risk budget and placing a strong focus on credit risk selection, Asian Short Duration strategy can help to provide relative insulation from potential macro shocks.

Low interest rates send yield hunters east

The COVID-19 pandemic has exacerbated the many structural challenges facing fixed income investors.

For one, global interest rates had fallen to near zero even before the latest crisis, limiting central banks’ options for more monetary support. The room for conventional policies in most developed countries had been exhausted during the global financial crisis, with successive rounds of quantitative easing (QE) further suppressing bond market term premiums, making it difficult to sustain returns.

Some central banks, in the euro area and Japan for example, have even gone a step further into negative interest rates, giving rise to the peculiar asset class of “negative-yielding” bonds – a sector which has grown to almost $15 trillion in size1 . In today’s zero-rate environment where finding yield has become increasingly challenging, it’s inevitable for global bond investors to venture out of their comfort zones into markets with higher credit risks, in a bid to find higher yields.

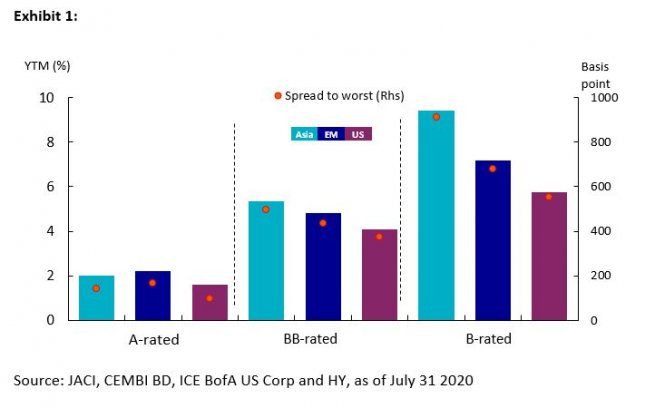

Right now, Asia’s credit market is attracting growing attention from global investors. The local currency universe has seen over 400% growth over the 10 years up to 2019, while over the same time period, the hard currency universe has experienced over 500% growth almost US$1.6 trillion.2 Greater potential growth in the region has historically sustained higher nominal interest rates, while Asian credit has both higher ratings - with corresponding lower defaults - and spreads than their US and European peers, meaning they are offering potentially better rewards to investors. (Exhibit 1)

- aHR0cHM6Ly93d3cuYmxvb21iZXJnLmNvbS9uZXdzL2FydGljbGVzLzIwMTktMDgtMDYvbmVnYXRpdmUteWllbGRpbmctZGVidC1oaXRzLXJlY29yZC0xNS10cmlsbGlvbi1vbi10cmFkZS13b2VzIEF1ZyA2LCAyMDE5

- IFNvdXJjZTogQVhBIElNLCBBc2lhbiBEZXZlbG9wbWVudCBCYW5rLCBBc2lhbiBCb25kIE1vbml0b3IgTWFyY2ggMjAyMC4gTWFyIDIwMTkgZGF0YSBmb3IgTG9jYWwgQ3VycmVuY3kgYW5kIFNlcHRlbWJlciAyMDE4IGZvciBGb3JlaWduIEN1cnJlbmN5IChsYXN0IGNvbXBsZXRlIHNldCBvZiBkYXRhKS4=

Lower for longer? Short duration can help investors tackle rising inflation and long-term interest rate risks

Rising interest rates pose a significant challenge to any fixed income portfolio, and even a threat of large drawdowns in value, particularly to those with longer duration. While no major central banks are in the position to lift policy rates while COVID-19 remains uncontained, long-term bond yields bear little resistance should inflation rebound, and bond supply concerns rise. US 10-year Treasury yields rose 20 basis points in August 2020, while the breakeven inflation rate – a measure of market inflation expectations – surged to 1.75% from a low of 0.6% at the height of the COVID crisis in March 20203 .

If the Federal Reserve was successful in stoking inflation with its latest change in mandate to keep policy rates lower for longer, even as inflation returns to the economy, a further rise in inflation

expectations could push nominal bond yields even higher. This in turn could cement a turning point in the global interest rate cycle.

A short duration strategy can provide a natural shield against higher inflation and interest rates. Contrary to any tactical moves to position for rising or falling rates, our Asian Short Duration strategy lies in its systematic approach to manage duration, structurally limiting it to under three years. Such a design feature is not motivated by our cyclical view of the interest rate cycle but is more of a strategic choice. It reflects our preference for focusing on yield and return from credit exposure over extended duration.

With global interest rates already at the zero-lower bound, the chance of a continued fall is less than that of flat or even rising interest rates. In our view, where we are currently in the interest rate cycle is playing in favour of a short duration fixed income strategy.

Strong credit focus can provide relative insulation from macro uncertainties

It’s important for investors to be aware that we are facing a series of elevated, and likely protracted, macroeconomic uncertainties. The pandemic, which has already had an historically negative impact on the global economy, has also further increased tensions between China and US. Clearly US election politics are not helping to cool the rhetoric with China. The uncertainties with such a consequential presidential election, between two drastically distinctive candidates with starkly different policy preferences, will also have global markets repositioning as Election Day draws closer.

As such, over the near and medium terms, geopolitical uncertainty is likely to challenge investors’ risk management by either increasing volatility over anticipation of negative events or creating further price shocks from actual negative events, as witnessed in March 2020. We believe an active Asian credit strategy such as Asian Short Duration is potentially well suited for these challenges.

Even with the COVID-19 impact and persistently ominous headlines throughout much of 2020, it is important to reflect that the direct impact on much of the Asian credit universe has been well contained and that the previously impacted sectors in the market have rallied and substantially recovered most losses. Going forward, we believe that with a strong emphasis on active credit research, focused credit selection can help effectively mitigate many of the ongoing macro uncertainties facing investors and continue to generate stable investment returns.

Looking ahead

There’s no doubt that recent developments in a constantly evolving global environment have presented some formidable challenges for fixed income investors. Zero interest rates and threats of inflation are undermining returns, while a long list of geopolitical tensions, particularly between China and the US, are adding to an uncertain environment for financial markets globally. A portfolio that can generate stable yield, while managing volatility and risks, particularly against those of rising interest rates, could provide an effective solution.

Designed to tap a large, diverse and rapidly growing bond market, supported by Asia’s vibrant economies and prudent policies, we believe the considerable merits of an Asian Short Duration strategy are especially appealing in today’s complex, uncertain and fast-changing world.

- U291cmNlOiBCbG9vbWJlcmc=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Risk Warning

The value of investments, and the income from them, can fall as well as rise and investors may not get back the amount originally invested.